Dividend payout:

A dividend is a share of profits in the fund paid out to you periodically. Assuming you have 100 units in your MF and the face value of each unit is Rs 10. Now, the fund house declares 50% dividend on the scheme. So, for every unit you will get Rs 5 (50% of Rs 10), that is Rs 500 for 100 units.

You might rejoice at the thought of getting some extra money periodically, but the catch lies in the fact that the NAV of the unit will fall by the amount of the dividend declared. This means, if the dividend paid out is Rs 5 and if the NAV were Rs 15 before dividend declaration, the NAV will fall to Rs 10. In other words, your own money is paid back to you in a different way. It is called the dividend payout option.

Tax implication:

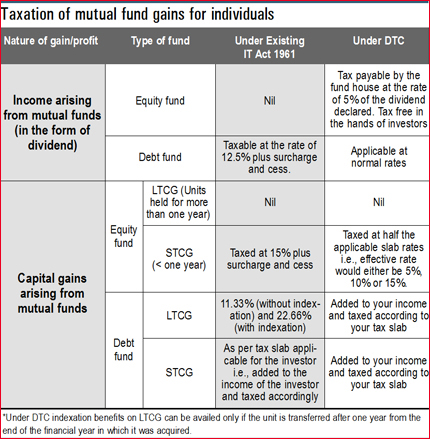

The dividends received in equity funds, balanced funds (funds with more than 65% in equity) and debt funds are tax-free in the hands of the investor.

Dividend reinvestment:

You might rejoice at the thought of getting some extra money periodically, but the catch lies in the fact that the NAV of the unit will fall by the amount of the dividend declared. This means, if the dividend paid out is Rs 5 and if the NAV were Rs 15 before dividend declaration, the NAV will fall to Rs 10. In other words, your own money is paid back to you in a different way. It is called the dividend payout option.

Tax implication:

The dividends received in equity funds, balanced funds (funds with more than 65% in equity) and debt funds are tax-free in the hands of the investor.

Dividend reinvestment:

In this option, the dividend paid out by the fund is ploughed back into the same scheme. Let's understand this with the same example described above. Instead of paying out the Rs 500 as dividend, the same will be reinvested, that is, it will be used to buy new units. This means, you will have additional units in your fund.

Tax implication:

Since dividends are tax-free in the investor's hands, the only tax impact here will be that of capital gains. In case of equity funds, if you sell units under this option within 1 year you will have to pay 15% short term capital gains tax. If you sell the units after 1 year, there is no tax. For this, the time period is calculated separately for each dividend reinvested.

In debt funds, you will have to pay tax according to your tax slab if you sell within a year, and long term capital gains tax at 20% if you sell after a year.

In this option you also get the benefit of tax deduction on dividends reinvested. This applies only in case of ELSS schemes. The dividends reinvested would be considered as an additional investment under section 80C.

Growth:

Tax implication:

Since dividends are tax-free in the investor's hands, the only tax impact here will be that of capital gains. In case of equity funds, if you sell units under this option within 1 year you will have to pay 15% short term capital gains tax. If you sell the units after 1 year, there is no tax. For this, the time period is calculated separately for each dividend reinvested.

In debt funds, you will have to pay tax according to your tax slab if you sell within a year, and long term capital gains tax at 20% if you sell after a year.

In this option you also get the benefit of tax deduction on dividends reinvested. This applies only in case of ELSS schemes. The dividends reinvested would be considered as an additional investment under section 80C.

Growth:

Unlike the payout or reinvestment, growth option doesn't pay you any dividends. Instead the price appreciation reflects in the NAV. So, if a fund appreciates by 5%, the growth fund NAV will go up from say Rs 10 to Rs 15.

Tax implication:

In growth funds the important tax to consider is capital gains tax, that is, the tax that is charged on profits from sale of the units. Capital gains tax will be the same as that of dividend reinvestment option.

A point to note: In case of debt funds, there is a dividend distribution tax that the fund house has to pay on dividends declared. While there is no tax in the hands of the investor, this DDT will have a bearing on the returns. So a growth option would score over a dividend reinvestment option in case of debt funds, because if you choose a reinvestment option, you would be bearing tax on the dividends (although indirectly) and then capital gains tax as well.

How to choose:

Your need and the tax implication are the two main deciding factors. Here's a matrix to help you choose:

- Periodic cashflows + debt fund = Dividend option

- Periodic cashflows + equity fund = Dividend option

- No periodic cashflows + debt fund = Growth option

- No periodic cashflows + equity fund = Growth or dividend reinvestment option (watch out for short-term capital gains tax in case of dividend reinvestment option)

Source: Economic Times by Deepa Venkatraghvan

Tax implication:

In growth funds the important tax to consider is capital gains tax, that is, the tax that is charged on profits from sale of the units. Capital gains tax will be the same as that of dividend reinvestment option.

A point to note: In case of debt funds, there is a dividend distribution tax that the fund house has to pay on dividends declared. While there is no tax in the hands of the investor, this DDT will have a bearing on the returns. So a growth option would score over a dividend reinvestment option in case of debt funds, because if you choose a reinvestment option, you would be bearing tax on the dividends (although indirectly) and then capital gains tax as well.

How to choose:

Your need and the tax implication are the two main deciding factors. Here's a matrix to help you choose:

- Periodic cashflows + debt fund = Dividend option

- Periodic cashflows + equity fund = Dividend option

- No periodic cashflows + debt fund = Growth option

- No periodic cashflows + equity fund = Growth or dividend reinvestment option (watch out for short-term capital gains tax in case of dividend reinvestment option)

Source: Economic Times by Deepa Venkatraghvan

.....png)

.....png)